TL;DR

- Under section 20 of the Nigeria Tax Act 2025, business expenses are generally deductible when they are "wholly and exclusively" incurred to produce your income.

- Under section 21, you do not get a deduction for "domestic or private expense", capital expenditure, fines, or profit taxes.

- Recurring creator costs like domain renewals, hosting, Render/Vercel, Adobe/Canva, business data, coworking, contractor fees, bank charges, and repairs will usually be easier to deduct than big asset purchases.

- Big-ticket items like laptops, cameras, generators, phones, cars, furniture, and purchased software are usually not deducted all at once. They are often claimed through capital allowance instead.

- If you cannot prove it with invoices, receipts, contracts, logs, or other records, do not expect the tax authority to be kind.

Here’s something many creators do not realize until tax season gets uncomfortably close: you can spend money all year to keep your work moving and still overpay tax because you did not know what counts, what does not, and what belongs in a different bucket.

Think about a normal month:

- you renew a domain

- you pay Render or Vercel

- you top up data

- you fuel the generator because NEPA picked the worst possible time

- you pay an editor, designer, or developer

Those are not random lifestyle costs. They are usually part of the cost of earning your income.

But the minute you start mixing in private spending, or you buy something big like a laptop, camera, or car, the answer changes.

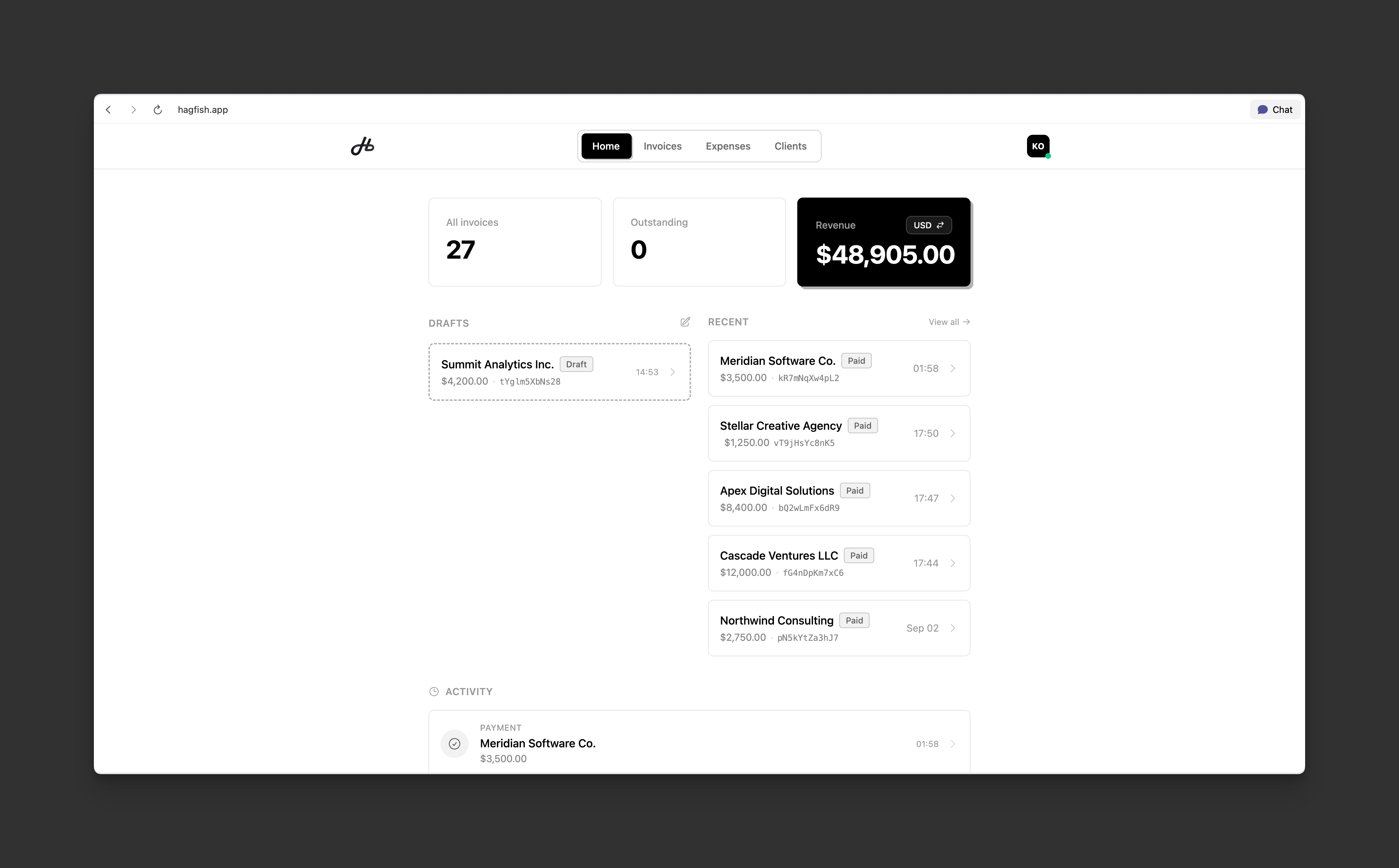

This is also where Hagfish can quietly save you stress. Most people do not lose deductions because the law hid them. They lose them because they did not track the expense properly when it happened.

When you log an expense in Hagfish, you can mark it as a Business expense, and Hagfish now auto-fills Tax deductible defaults based on the expense category. Then, when tax time comes, Hagfish can pull together the expenses already marked as deductible instead of forcing you to reconstruct the whole year from bank alerts and half-remembered subscriptions.

The rule in plain English

This post is about the part of the new law that applies to profits from a trade, business, profession, or vocation. That is the bucket most freelancers, creators, consultants, developers, designers, editors, coaches, and one-person studios fall into.

The easiest way to think about the new Act is this:

- If the expense exists because your business exists, it is usually easier to defend.

- If the expense also clearly serves your personal life, it becomes weaker and usually needs apportionment.

- If the expense buys you a long-term asset, it is usually a capital-allowance question, not a normal expense deduction.

That is really the whole game.

The law is helpful in one direction and strict in another:

- Section 20 opens the door for normal operating costs.

- Section 21 closes the door on private spending, capital spending, fines, and similar items.

So the real question is not just, "Did I spend money?"

It is, "What kind of spend was this?"

Green light: expenses creators can usually deduct now

These are the expenses most creators and freelancers can usually defend without drama, as long as the spending is genuinely tied to work and properly documented.

Domains, hosting, cloud tools, and web infrastructure

If your website, client portal, portfolio, ecommerce site, or course platform helps you earn income, the day-to-day cost of keeping it online is usually a normal business expense.

Examples:

- domain renewal for your portfolio or product site

- hosting on Namecheap, Hostinger, DigitalOcean, Hetzner, or cPanel hosting

- a VPS on Hetzner for your app, site, or client projects

- Render, Vercel, Netlify, Railway, Cloudflare, or Supabase subscriptions

- SSL certificates, email hosting, CDN fees, transactional email, and uptime monitoring tools

Example:

You run a paid newsletter and landing page for sponsorship deals.

- Domain renewal:

₦45,000 - Hetzner VPS:

€4.51/month - Render:

$7/month - Postmark:

$15/month

That is the kind of spending the law is usually more comfortable with. You are not building a personal luxury here. You are paying to keep the thing that earns you money alive.

Important nuance:

- A normal domain renewal is easier to defend as a current expense.

- Buying an expensive premium domain that you intend to hold long term is more likely to raise a capital-vs-expense question.

Software subscriptions

Recurring software costs are one of the cleanest deductions for modern creators and freelancers.

Examples:

- Adobe Creative Cloud

- Canva Pro

- Figma

- Notion

- Descript

- CapCut Pro

- Riverside

- Loom

- Dropbox

- Google Workspace

- ChatGPT or other AI tools used for work

If you pay monthly or annually to access a tool you use to produce deliverables, manage projects, edit content, host files, or run client work, it will usually sit comfortably inside the section 20 logic.

Example:

A video editor pays for:

- Adobe Creative Cloud

- Frame.io

- Dropbox

- music licensing libraries

Nobody pays for those tools for fun. They are part of the machine.

Internet, data, phone, and communication tools

For many Nigerian freelancers, internet is not optional. It is the business.

Examples:

- Starlink subscription

- fiber broadband

- MTN/Glo/Airtel mobile data or Starlink top-ups for uploads and client work

- Zoom, Meet, or VoIP tools

- business phone line

If you use one connection for both work and personal life, claim only the business share.

Example:

You spend ₦80,000 monthly on internet and can reasonably show that about 75% of usage is for client calls, uploads, editing sync, and project delivery.

Your more defensible deduction is the business portion, not the full household number.

Studio, office, and coworking rent

Section 20(b) specifically allows rent and premiums on land or buildings occupied to generate income.

Examples:

- coworking membership

- studio rent

- office rent

- rehearsal space

- shared editing suite

- podcast room rental

Example:

You are a photographer paying:

₦250,000/monthfor a small studio₦40,000/monthfor storage of props and backdrops

Those are far easier to defend than claiming your entire home rent.

Contractors, collaborators, and outsourced work

If you pay other people to help produce the work you sell, those payments are usually ordinary business expenses.

Examples:

- editor

- thumbnail designer

- copywriter

- motion designer

- VA

- developer

- community manager

- sound engineer

- makeup artist hired for a shoot

Example:

A YouTube creator pays:

₦120,000to an editor₦35,000to a thumbnail designer₦60,000to a script researcher

These are usually easier to deduct than buying a new camera body.

Payment processing fees, bank charges, and business admin costs

Creators lose money here quietly all year and forget it at tax time.

Examples:

- Paystack charges

- Flutterwave charges

- Stripe Atlas-related operational fees

- bank transfer charges on the business account

- accountant fees

- bookkeeping software

- invoicing software

- tax filing support

- legal fees for client contracts or collections

If it is a cost of getting paid, staying compliant, or keeping the business in motion, it is often deductible.

Repairs and maintenance

Section 20(d) is useful here. It allows repair costs for premises, plant, machinery, or fixtures used to generate income.

Examples:

- servicing your generator used in your studio

- fixing a camera lens

- repairing a work laptop screen

- replacing a UPS battery used for your editing setup

- repairing office AC in a studio you use for work

Repairs are easier than upgrades.

Example:

- Fixing your current mic: usually a repair expense

- Buying a brand new premium mic: more likely capital expenditure

Pre-launch expenses before the business properly starts

One underrated part of section 20(j) is that certain expenses incurred within six years before commencement may be treated as if they were incurred on the first day of business, if they would have been deductible after launch.

That matters because a lot of creators spend before they officially "start."

You buy the domain first. You pay for the first tools first. You test the idea first.

Then the income comes later.

Example:

You spent money before launch on:

- your domain

- early hosting

- test subscriptions

- logo design

- market validation tools

If those expenses are of the kind that would normally be deductible after launch, section 20(j) may help.

Bad debts from clients who do not pay

Section 20(h) allows bad or doubtful debts in certain cases.

This matters if:

- you invoiced the client

- the debt genuinely went bad

- it is not a related-party game

- you can prove the history

Example:

You delivered a branding project for ₦600,000, recognized the revenue, chased the client for months, and the receivable became unrecoverable.

That is not the same thing as simply failing to collect a deposit. It is a bad-debt issue and can matter in your tax computation.

Yellow light: deductible, but only if you handle it carefully

These are the expenses people love to over-claim.

Fuel, diesel, electricity, and generator costs

Yes, these can be deductible.

But only to the extent they are tied to work.

Examples that are easier to defend:

- fuel for a generator powering your editing suite during outages

- diesel for a studio shoot

- fuel for driving to a paid shoot, client meeting, or content production day

- electricity costs for a dedicated studio or office

Examples that are harder:

- general family generator fuel

- everyday commuting

- personal errands mixed with work

Example:

You are a freelance videographer and keep a simple log showing:

₦180,000generator fuel for edit sessions and render nights₦95,000car fuel for client shoots

That is far more defensible than simply throwing your full monthly fuel spend into a spreadsheet and calling it business.

Home internet, home electricity, and home rent

This is the classic mixed-use zone.

You may have a reasonable claim to the business portion, but this is where people get sloppy and overstate.

Safer approach:

- use a dedicated workspace if possible

- use a conservative percentage

- write down how you arrived at the split

- keep the bills

Example:

If you work from home and estimate that 30% of your electricity supports your editing station, router, lights, and work equipment, that is more defensible than claiming 100%.

Important distinction:

- business rent for a studio, office, or coworking setup sits under section 20(b)

- personal rent relief for individuals is a separate rule under section 30(2)(a)(vi), capped at

20%of annual rent paid and at₦500,000, whichever is lower

If you want to claim both a business-use share of home rent and the separate personal rent relief on the same rent, get proper advice first. That is not a place to improvise.

Education, courses, books, and conferences

These can be defensible when they are directly tied to your current income-producing work, but they are not as clean as rent, software, or contractor fees.

Stronger cases:

- a motion designer paying for a paid After Effects masterclass used in active client work

- a tax consultant paying for a professional compliance update

- a creator paying for a course on ad operations for a monetized channel

Weaker cases:

- broad self-improvement

- hobby learning

- a long academic programme not clearly tied to current business income

Keep the invoice and keep a short note explaining the business purpose.

Clothes, makeup, grooming, and appearance

This is one of the easiest places to get carried away.

Usually weak:

- everyday clothes

- grooming

- haircuts

- beauty treatments

- normal makeup for personal presentation

Potentially stronger, but still sensitive:

- wardrobe bought solely as costumes or props for a production

- protective gear used only for a specific production environment

As a simple rule, if you would still buy it even if you had no clients, no audience, and no business, the claim is usually weak.

Red light: things you usually should not deduct

Section 21 is blunt here.

Usually non-deductible:

- your personal groceries

- family rent unrelated to business use

- school fees

- personal shopping

- profit taxes and similar taxes on income

- fines and penalties

- private travel

- private fuel

- spending on assets not used for the business

Examples:

- speeding fine on your way to a client shoot: not deductible

- your own income tax payment: not deductible

- weekend clothes bought because you are "a creator": usually not deductible

- your partner's phone bought with no business role: not deductible

Also important:

- section 21(p) says expenses can run into trouble where VAT was due but not charged, or import duty/levy should have been paid but was not

That means messy paperwork is not a harmless detail.

Big purchases are different: claim capital allowance instead

This is the part many freelancers miss, and it is where a lot of confusion starts.

The new Act generally blocks direct deduction for capital expenditure under section 21(b). But for both companies and individuals, the Act also allows capital allowance through the First Schedule and section 28(2)(b)(ii).

In practical terms:

- recurring expense today: usually section 20

- long-term asset: usually capital allowance

The official table in the First Schedule groups capital allowance classes like this:

| Class | Rate | Broad categories in the Act |

|---|---|---|

| 1 | 10% | Building, agricultural expenditure, mast expenditure, intangible assets, heavy transportation |

| 2 | 20% | Plant expenditure, agricultural equipment, furniture and fittings, mining expenditure, other equipment |

| 3 | 25% | Motor vehicles, software, other capital expenditure |

Practical mapping for creators and freelancers:

| Asset | Likely treatment | Practical note |

|---|---|---|

| Laptop, camera, lighting kit, generator, inverter, printer | Usually capital allowance, often closest to plant or other equipment | Usually not a full one-year expense deduction |

| Desk, chair, shelves, studio furniture | Usually capital allowance | Furniture and fittings are in the schedule |

| Car used for client visits or shoots | Usually capital allowance | Be conservative on mixed personal use |

| Purchased software or perpetual licence | Usually capital allowance | The schedule expressly includes software expenditure |

Important nuance:

- The asset mapping above is a practical inference from the First Schedule categories, not a substitute for asset-by-asset professional classification in complex cases.

- If an asset is partly personal and partly business, only the business portion is the safer claim.

Examples that make the rule real

Example 1: domain, Render, Adobe, fuel, and internet

A freelance designer earns ₦9,000,000 in the year and incurs:

- domain renewal:

₦40,000 - Render:

$7/month - Adobe Creative Cloud:

₦55,000/month - business data and internet share:

₦720,000 - generator fuel for late-night production work:

₦240,000 - coworking:

₦1,200,000 - contractor illustrator:

₦600,000

Those are generally the kind of recurring costs that are easier to defend under section 20, assuming the records are clean.

Example 2: laptop and camera

The same designer buys:

- MacBook:

₦2,100,000 - camera:

₦1,300,000

This is where a lot of people make the wrong move.

They think, "I bought it for work, so I should deduct everything this year."

But these are long-term business assets, so the better question is capital allowance, not immediate full deduction.

The same logic usually applies if you invest in:

- a solar setup for your studio

- an inverter and battery system for your work setup

- a new generator used to keep production running

Those are often real business costs, but they are usually closer to equipment or plant than to an ordinary recurring expense.

Example 3: bad debt

A creator invoices a Nigerian brand ₦850,000, delivers the campaign, records the receivable, follows up for months, and eventually concludes the debt is bad.

That can be a tax issue under the bad-debt rule, not just a painful business story.

Example 4: paying in dollars

You pay for:

- Framer in USD

- ConvertKit in USD

- Google Workspace in USD

Under section 20(4), foreign-currency expenses are deductible only to the extent of their naira equivalent at the official CBN exchange rate for the relevant date or period.

So do not just type "roughly ₦whatever" from memory at year end.

How Hagfish helps you track this without overthinking it

Hagfish already does something useful here today.

On the expense form:

- if you turn Business expense off, Hagfish forces Tax deductible off too

- if you leave Business expense on, Hagfish uses the category to prefill a likely deductible direction

- you can still override the default when your situation needs it

That is the right level of product help.

It speeds up capture without pretending the app is doing full legal analysis for you.

Categories that currently default to tax deductible

Today, Hagfish defaults these categories to tax deductible:

- software

- subscriptions

- rent

- office supplies

- internet and phone

- bank fees

- contractors

- professional services

- repairs and maintenance

- utilities

- travel

- transport

- marketing

That is useful because these are the categories creators and freelancers most often mean to claim, but still forget to classify properly.

You should not have to do mini tax analysis from scratch every time you pay MTN, coworking, Paystack, or a contractor.

Categories that currently default to not tax deductible

Today, Hagfish defaults these categories to not tax deductible:

- equipment

- meals

- entertainment

That is also sensible.

These are exactly the kinds of expenses where people overclaim too easily, or where the better answer may be capital allowance instead of a simple same-year deduction.

Categories Hagfish leaves manual

Today, Hagfish leaves these manual:

- education

- insurance

- other

That is a good tradeoff because these often need context.

An editing course may be easier to defend than broad personal development. Insurance may be business-related or personal. Other is too vague to guess safely.

Important nuance

These are smart defaults, not guarantees.

They help you classify faster, but they do not replace judgment.

That matters for mixed-use or context-heavy spending like:

- fuel

- home rent

- household electricity

- solar, inverter, or generator purchases

Those may be very real business costs, but they often need either:

- a business-use split, or

- a capital-allowance treatment instead of a simple current expense deduction

Why this matters

This kind of feature does two useful things at once.

First, it reduces friction. A user logging 40 expenses in a month should not have to do tax interpretation from scratch on every row.

Second, it improves the quality of the data Hagfish uses later in the tax assistant. If the expense categories and deductible flags are cleaner during capture, the year-end tax summary becomes far more useful.

That is the real promise.

Not: "Hagfish files your taxes by guessing."

But: "Hagfish helps you capture expenses in a way that is much closer to filing reality."

That may sound small, but it is the difference between showing up at filing time with a usable record and showing up with a vague memory of what that debit alert was for.

The receipts and records you should keep

The new Act is generous to genuine business spending, but it is not casual about proof.

For individuals, section 31 says deductions must be claimed in writing, and section 32 lets the tax authority ask for "documentary evidence" and refuse claims where the evidence is missing or inadequate.

Keep:

- invoices

- receipts

- payment confirmations

- contracts

- simple mileage or fuel logs

- internet or utility apportionment notes

- asset purchase documents

- VAT-inclusive invoices where applicable

- import paperwork for imported equipment

- FX conversion support for USD charges

- debt recovery correspondence for bad-debt claims

If your records are a mess, the law gives the authority room to fall back on a presumptive approach under section 29.

That is another way of saying: bad records can get expensive.

A simple creator checklist

Before you claim an expense, ask:

- Did I incur this because I was earning business income?

- Is it private, mixed, or purely business?

- Is it a recurring operating cost or a long-term asset?

- Do I have clean proof?

- If it is mixed-use, have I used a conservative split?

- If it is a big asset, should I be thinking capital allowance instead?

Final thought

The new Nigeria Tax Act 2025 is actually pretty clear on the core idea: ordinary business-running costs are deductible, private spending is not, and assets live in a different bucket.

For creators and freelancers, the tax savings are usually hiding in boring places:

- domain renewals

- hosting

- Render or Vercel

- software subscriptions

- internet

- fuel tied to production

- contractor fees

- coworking

- repairs

- bank and payment charges

Miss those and you overpay tax.

But the bigger mistake is the opposite one: treating your entire life as a business deduction just because you post online or work for yourself.

The winning move is not aggressiveness. It is clean classification.

And that is really the nudge here: do not wait until year end to figure this out. Track the expense when it happens. Mark whether it is a business expense. Let Hagfish prefill the obvious deductible categories. Attach the receipt while it is still in your WhatsApp or email.

If you already use Hagfish, use that workflow as you go, not as a cleanup exercise in March. That is where the real tax win is.

Sources used

- Nigeria Tax Act, 2025 (official PDF hosted by NIPC)

- NIPC Compendium of Investment Incentives: Tax-Based Incentives under the Nigeria Tax Act 2025

Related reading: